You have actually most likely seen the commercials on television: A pitchman claims that you can resolve your tax expense for “pennies on the dollar.” All you need to do is work with the law firm in the business and also they will certainly use their special negotiating skills as well as inside knowledge to get you off the hook with the Internal Revenue Service (IRS). Is this true? Does the IRS Really Settle for Less?

In the real world, however, it’s not so very easy to get the IRS to work out a tax financial obligation for pennies on the dollar. It does take place, however only in cases where a taxpayer clearly does not have the assets and/or income to pay off the tax obligation financial obligation in a reasonable time. If you have the cash to pay the IRS– or will likely have it in the future – no quantity of negotiating will certainly encourage the IRS to settle for less than you owe. This is so whether you represent yourself or hire an expensive law firm.

Does the IRS Really Settle for Less?

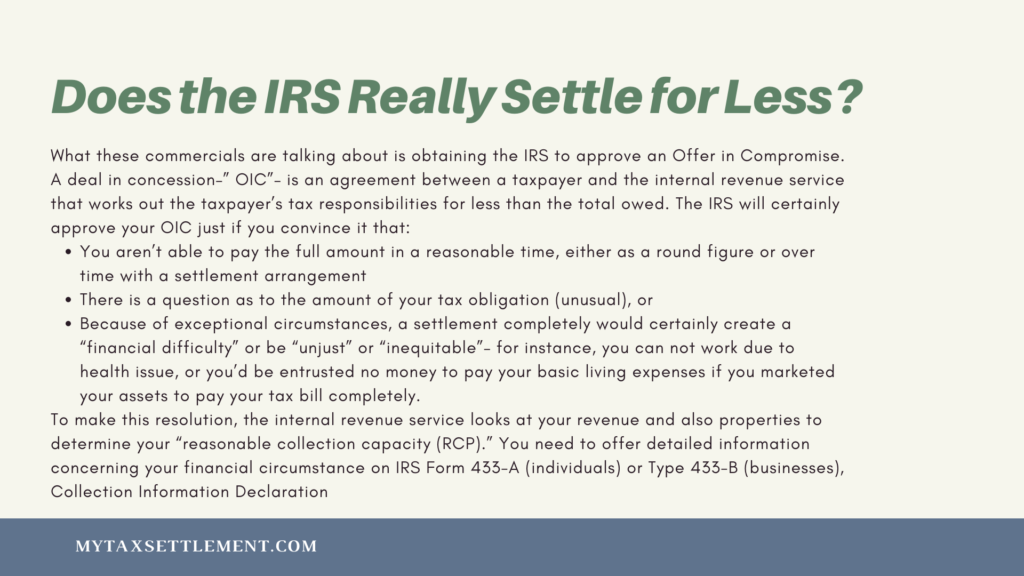

What these commercials are talking about is obtaining the IRS to approve an Offer in Compromise. An Offer in Compromise – “OIC” – is an agreement between a taxpayer and the internal revenue service that works out the taxpayer’s tax responsibilities for less than the total owed. The IRS will certainly approve your OIC just if you convince it that:

- You aren’t able to pay the full amount in a reasonable time, either as a round figure or over time with a settlement arrangement

- There is a question as to the amount of your tax obligation (unusual), or

- Because of exceptional circumstances, a settlement completely would certainly create a “financial difficulty” or be “unjust” or “inequitable”– for instance, you can not work due to health issue, or you’d be entrusted no money to pay your basic living expenses if you marketed your assets to pay your tax bill completely.

To make this resolution, the internal revenue service looks at your revenue and also properties to determine your “reasonable collection capacity (RCP).” You need to offer detailed information concerning your financial circumstance on IRS Form 433-A (individuals) or Type 433-B (businesses), Collection Information Declaration. This consists of proven info about your cash, financial investments, readily available debt, properties, revenue, and also financial debt. Along with property, the RCP likewise includes your anticipated future earnings, much fewer amounts allowed for basic living costs. You can make use of the Offer in Compromise Pre-Qualifier on the IRS website to determine whether you are eligible and prepare an initial proposal.

You will certainly need to find up a minimum offer amount as part of your OIC. This is the minimum. quantity the internal revenue service will accept as well as is based on the monetary disclosures you make in your Kind 433. Basically, your offer has to equate to the net realizable value of your possessions plus your excess regular monthly earnings after subtracting your month-to-month costs. You then increase this number by 12 or 24, depending upon which payment period you pick (either five months or more years). You can comply with the directions in Type 433 for determining your minimum offer.

Before you submit your deal, you have to

- File all income tax returns you are legitimately required to submit,

- Make all needed estimated tax obligation settlements for the current year, and also

- Make all needed government tax deposits for the present quarter if you are a company owner with employees. If you or your organization is presently in an open personal bankruptcy proceeding, you are not eligible to get an offer. Your debts need to be fixed in your bankruptcy proceeding– that’s what personal bankruptcy is for.

The OIC Pamphlet, Form 656-B (PDF) has step-by-step directions for preparing and also sending all the necessary kinds for an OIC. You don’t have to employ a law practice or other tax obligation expert to make an OIC. If your offer is rejected, you can appeal within 30 days using Request for Appeal of Rejected Offer in Compromise.

Further Reading

-

How Much Should I Offer in Compromise to the IRS?

If you cannot pay your tax debt, you can try to settle with the IRS for less than what you owe. If successful, a partial payment arrangement or offer in compromise may be an option. An offer in compromise is a settlement agreement between a taxpayer and the IRS that allows taxpayers with financial hardship to resolve their tax debts for less than the full amount owed. The Offer In Compromise program becomes an option when other collection efforts have proven unsuccessful and allow you to settle your tax debt for less than what you owe. Here are some questions and answers about OICs…

-

How Much Will the IRS Usually Settle for? A Closer Look at Offers in Compromise

How Much Will the IRS Usually Settle for? Each year, the Internal Revenue Service (IRS) approves countless Offers in Compromise with taxpayers regarding their past-due tax payments. Basically, the IRS decreases the tax obligation debt owed by a taxpayer in exchange for a lump-sum settlement. The average Offer in Compromise the IRS approved in 2020 was $16,176. How do we get to that amount? In 2020, the IRS accepted 17,890 Offers in Compromise with a total worth of $289.4 million (resource). Divide $289.4 million by 17,890, and – presto! – you get an average deal in compromise of $16,176. Naturally, that number is meaningless…

-

Does the IRS Really Settle for Less?

You have actually most likely seen the commercials on television: A pitchman claims that you can resolve your tax expense for “pennies on the dollar.” All you need to do is work with the law firm in the business and also they will certainly use their special negotiating skills as well as inside knowledge to get you off the hook with the Internal Revenue Service (IRS). Is this true? Does the IRS Really Settle for Less? In the real world, however, it’s not so very easy to get the IRS to work out a tax financial obligation for pennies on the dollar. It does take place…